Como montar uma carteira de investimentos diversificada com maior retorno e menor risco?

Conheça o pai da Teoria Moderna de Portfólio

Harry Max Markowitz foi um dos principais economistas Americanos. Criou uma metodologia para calcular o risco versos retorno de uma carteira de investimentos, independente do tipo de ativos que a compõem. A metodologia ficou conhecida como Modelo de Markowitz.

Harry Markovitz nasceu em Chicago, EUA (24/8/1927 – 22/6/2023). De família judia. Desenvolveu interesse em física e em filosofia durante seus primeiros anos de estudo. Ingressou Universidade de Chicago, concluindo o curso de Economia.

Foi membro da Cowles Commission for Research in Economics, grupo de pesquisas em economia, fundado por Alfred Cowles, economista e empresário Americano, (15/9/1891 – 28/12/1984).

Em seus estudos, Markowitz trabalhou com a aplicação da matemática para a análise do mercado de ações. Identificou que o modelo aplicado na época para análise do mercado de ações, Modelo do Valor Presente de John Burr Williams, não considerava o impacto de risco.

Decidiu desenvolver sua própria teoria de alocação de portfólio em condições de incerteza, introduzindo o risco, correlação, rentabilidade e diversificação de ativos. Publicou essa teoria em 1952, no Journal of Finance, que foi bem aceita pela acadêmia e o mercado financeiro.

Em 1989, Markowitz ganhou o prêmio John von Neumann Theory Prize e em 1990 foi laureado com o Prêmio Nobel de Economia.

Modelo de Markowitz

O modelo de Markowitz é conhecido como Teoria Moderna do Portfólio. Trata-se de uma teoria pela qual investidores adversos ao risco podem construir seu portfólio para obter mais retorno a partir de um determinado nível de risco de mercado.

Esse modelo permite encontrar o maior nível de retorno para um certo nível de risco ou menor nível de risco para um certo nível de retorno.

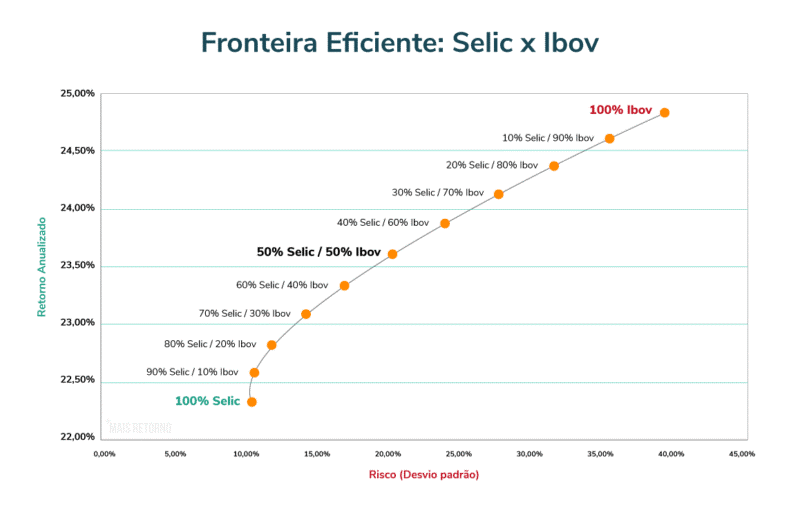

A base desse modelo é a construção de “fronteiras eficientes” de portfólios otimizados, considerando que risco e retorno devem ser avaliados em conjunto dentro da carteira de investimento.

Essas fronteiras eficientes são as combinações possíveis de ativos, apresentadas como pontos em um gráfico no qual o eixo X corresponde ao risco e o eixo Y corresponde ao retorno.

Os pontos são conectados, formando uma curva hiperbólica ascendente, que representa a fronteira mais eficiente. Dessa forma, o investidor consegue identificar com boa precisão qual é a combinação de ativos capaz de produzir o resultado mais eficiente.

Aplicação prática para o Investidor

Através do Modelo de Markowitz, o investidor consegue construir um portfólio onde o retorno individual de um certo ativo é menos importante do que o desempenho que ele apresenta no contexto da carteira de investimentos. Esse é o benefício da diversificação dos ativos.

O retorno do portfólio, no Modelo de Markowitz, é calculado por meio da soma ponderada do retorno dos ativos que compõem a carteira. Já o risco é calculado através das variâncias e correlações dos ativos. O Modelo de Markowitz revolucionou a maneira como as pessoas investem.

Os gestores de ativos e fundos utilizam o Modelo de Markowitz para selecionar os ativos e fazer a combinação da proporção ideal de cada ativo em seus portfólios e em suas carteiras de Fundos de Investimento.

Referências:

- W. Andrew e FOERSTER, Stephen R. Em busca do Portfolio Perfeito: as histórias, as vozes e os principais insights dos pioneiros que mudaram a forma como investimos. Ed.Alta Books.2021.

MARKOWITZ, Harry M. e BLAY Kenneth A. Risk – Return Analysis. The Theory and Practice of Rational Investing. Vol. I. Ed. Mc Graw Hill. 2014.